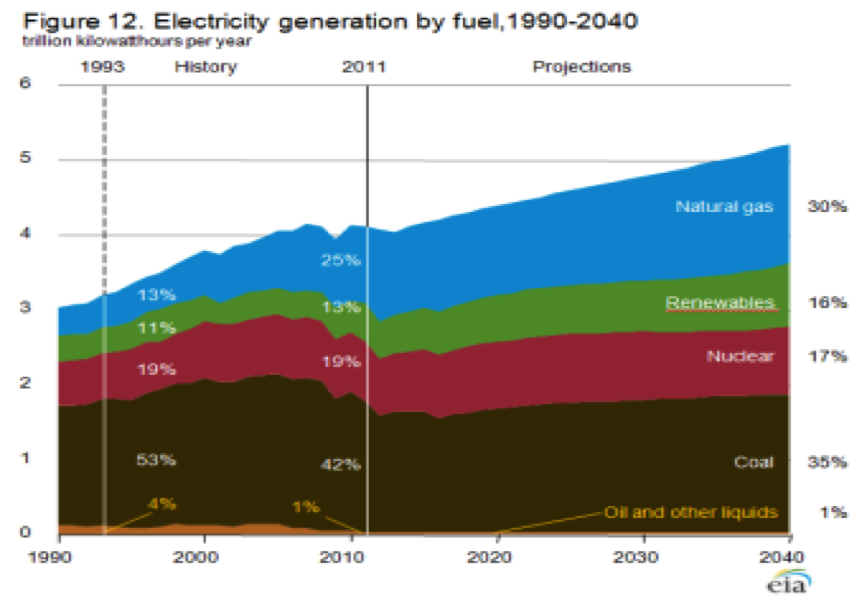

The EIA’s Annual Energy Outlook for 2013 projects a continuation of the rebalancing occurring in electricity generation in the USA (See figure 1), with gas rising to 30% of the US electricity mix by 2040. This switching of capacity from coal and nuclear power generation to gas generation is occurring already. For example, 2013 production estimates for electricity from natural gas are 10% higher than they were in previous estimates, with the difference driven by lower gas prices. Entergy has announced the retirement of their Vermont Yankee nuclear plant will occur in 2014, and falling wholesale electricity prices, caused by the natural gas boom, were blamed. Agitators for the Yankee plant’s shutdown noted; “natural gas is putting coal and nuclear out of business”.

Electricity generated from natural gas has its advantages, but inspection of natural gas prices shows significant volatility (see figure 2). Neither coal nor nuclear feedstock prices show such variability. Since 1995, the average year on year price change for natural gas was nearly 25% – compared with 15% for uranium and 10% for coal. For producers the difference is even more stark. Fuel costs for natural gas plants are greater as a share of total cost than for nuclear or coal. Adjusted for this exposure, the volatility in the price of gas has been approximately 18% of the total LCOE of gas plants each year – several times greater than the 2% for uranium and 3% for coal.

The high variability in gas prices is likely due in part to the market changes driven by the shale gas boom, but uncertainties remain which could continue to drive volatility. Environmental concerns continue to limit fracking licensing, hampering supply certainty, whilst federal permissions for LNG exports create ambiguity around long term demand. High variability in gas prices translates to high variability in the cost of gas-sources electricity.

Given this switch to gas, with its greater volatility in price, who should we expect to bear the costs and risks that come with higher reliance on natural gas? Will utilities pass this price volatility on to consumers? Or will the absorb all or some of it directly?

Or, can natural gas find its way to a stable equilibrium path, providing rising price and volume certainty to its end users?

EIA. (2012, December). Annual Energy Outlook, 2013. Retrieved from: http://www.eia.gov/forecasts/aeo/er/early_elecgen.cfm?src=Nuclear-b3

Smith, R. (2013, 13th Aug). Vermont Nuclear Plant’s Closure Shows Impact of Cheap Gas. Wall St Journal. Retrieved from:

http://online.wsj.com/news/articles/SB10001424127887323407104579038682331577924

Categories: Discussion - Oil & Gas, Electricity, Energy, Natural Gas

I don’t want to over-extrapolate, but gas prices are up 22% in the last month. Concerning to say the least…

http://www.infomine.com/ChartsAndData/GraphEngine.ashx?z=f&gf=110558.USD.mmbtu&df=20131101&dt=20131209

I think (or at least, I hope) that with the major health concerns there will be some kind of government intervention that will limit the fracking activity. Yes, it will adversely affect energy prices, but higher bills and a longer life somehow seem very appealing.

http://www.climatecentral.org/news/fracking-may-be-contaminating-river-with-radioactive-waste-16555

The IGU believes that the volatility of gas prices is even risky for LNG exports that link their prices to Henry Hub.

http://business.financialpost.com/2013/08/22/canadian-lng-projects-difficult-to-justify-report-says/

What will happen though, once the drilling technology matures and the efficiency improvements become less drastic. Will the number of rigs, based on a more stabilized efficiency again be a valuable indicator?