China has higher than average global energy costs, but is easily the world’s largest manufacturer of energy intensive products

Basically, China’s coal costs will make it less and less competitive on a global basis as it grows coal fired generation. We show a bottom up model of coal generation costs based on data from the Northern China Power University, which including interest and depreciation, but not tax or return on equity, are about $A75/MWh. We then sketch out a scenario where electricity consumption grows 3-4% per year for the next decade and non-thermal generation ends up with about 45-50%.

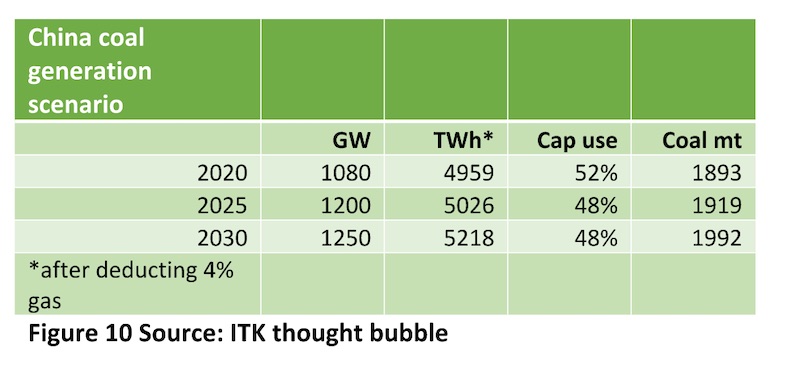

In our view, this is no different to what’s happening in other countries. In this scenario, coal generation remains close to flat, thermal coal demand increases by about 100 million tonnes, keeping cost pressure high and, assuming about 120GW of new capacity, coal generation capacity factors falls from about 52% to about 48%.

The coal generation industry would thus stay in the just-loss-making, just-profitable region, close to break even. Wind capacity would grow by an average 50GW per year and solar by over 60GW. We think these numbers are easily within China’s capability.

In the end, though, this is just a keyboard warrior scenario, albeit there’s some homework and a certain plausibility to it based on experience in other global markets and China’s can-do approach once a course is set.

Background

The key attributes of China’s coal electricity generation of interest to us are:

The close to 1 TW fleet is pretty new. The bulk is well less than 15 years old;

Capital costs are low, about A$0.7 m per MW, less than 1/3 of the costs in Australia;

Coal costs are very high. 5500 Kcal/kg coal typically sells for around 570 RMB/t = A$118/t;

The average coal plant is about 8% more efficient (GJ/MWh) than the average Australian plant. These are rough numbers but certainly Australian plants would have significantly lower energy costs per MWh than China plants;

Average capacity utilization is low (around 50%) and falling.

Putting these factors together, we estimate that plants need a price of around A$80-A$90/MWh to earn anything close to a return on equity. And in fact these numbers provide little error margin. Any slippage capacity use or higher coal prices kills profitability. On the other hand, we estimate that $A85 = $US60/MWh is already above the global average for where energy-intensive business needs to be. It’s about double what a globally competitive aluminium business wants, for instance. Low transmission costs may partly offset this generation cost disadvantage.

China is adding to its generation fleet, although the exact amount of growth is debatable. The best estimate, in my opinion, from University of Maryland School of Public Policy, Center for Global Sustainability, is that 151GW will be built over the next five years. However, some plant will probably be closed so the net increase will be smaller. Still, capacity is going to increase 10%-15%.

Of course, China is also rapidly adding to its wind and solar fleet and has made large growth in its nuclear fleet in recent years. So the economic question is whether there will be enough volume to make the new capacity profitable. Then there is a separate question of carbon emissions.

Economically, the simplest and most durable way to factor carbon in is to assume that, one way or another, policy will incentivise ongoing investment in wind, solar and even nuclear capacity. That’s what’s happening in virtually every geography around the world.

Capacity and capacity utilisation history

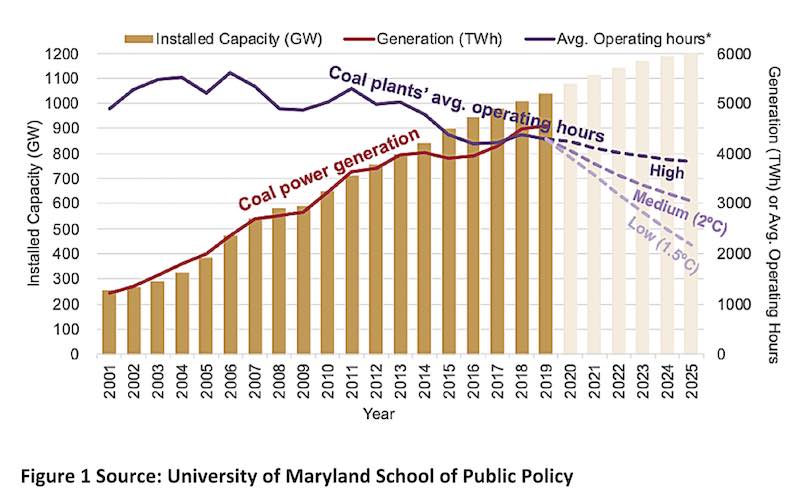

The figure below is taken from Implications of China coal build – University of Maryland and has more history than I could easily lay my hands on.

My focus is on the blue line (RHS) which shows operating hours, and by 2019 these were down to 4400 or so. That is, the average plant has capacity utilisation of 50%. In fact, according to the CEC, the average hours Jan-Aug 2020 for thermal plant were 2718, which I make to be 46% and down 3.9% on the same period a year earlier.

The fuel efficiency Jan-Aug 2020 worked to 306 g/KWh of “standard coal”. As near as I can work out, standard coal has 29 Gj/t, whereas 5500 Kcal/Coal has about 22 GJ/t of energy.

About 2016/17 North China Electric Power University [NPU]

Published with Greenpeace a study on the parameters for a standard new 600 MW coal power plant.

Published with Greenpeace a study on the parameters for a standard new 600 MW coal power plant.

To put that plant in context, it’s helpful to look at the entire China thermal fleet by fuel efficiency and year of going into service (vintage).

This remarkable graph shows the close to 80GW per year, that is more than 1500MW a week, that China installed in 2005 and 2006 and that perhaps 65% of the plant installed post 2005 is supercritical or better. Interestingly, there is not as much self-use (mainly aluminium) plant as I might have imagined.

This remarkable graph shows the close to 80GW per year, that is more than 1500MW a week, that China installed in 2005 and 2006 and that perhaps 65% of the plant installed post 2005 is supercritical or better. Interestingly, there is not as much self-use (mainly aluminium) plant as I might have imagined.

In any event, NPU’s model was based on 286g standard coal per KWh. That is actually a significantly higher standard than what China achieved in the first eight months of 2020 (306g), so it’s a reasonable modelling benchmark.

The history of the 5500 Kcal/KG “high quality” coal price in China is shown below…

…and shows that 550 RMB/t is a reasonable average price. So working that through, we get to a better than average China coal generator paying over A$40/MWh for coal:

Other variable costs were stated by NPU at 20 RMB/MWh or A$4/MWh and fixed costs of US$30 m = A$42 m. If capacity utilisation is 50% the fixed costs are about $A16/MWh, so now your total cash costs are $60/MWh and you still have to cover depreciation, tax, pay off the interest and the debt before you earn a return.

Other variable costs were stated by NPU at 20 RMB/MWh or A$4/MWh and fixed costs of US$30 m = A$42 m. If capacity utilisation is 50% the fixed costs are about $A16/MWh, so now your total cash costs are $60/MWh and you still have to cover depreciation, tax, pay off the interest and the debt before you earn a return.

We add it up to between $A72/MWh and $A78/MWh before tax. Note that the low capital cost is reflected in the low depreciation number. All the numbers have been expressed relative to volume to show, firstly, the influence of the capacity utilisation assumption and, secondly, that electricity costs in China at the generation level are very far from “cheap”.

The business is not particularly volume sensitive but the low level of capacity utilisation does make costs, say, 20% higher than they would be if capacity was better matched with demand.

The business is not particularly volume sensitive but the low level of capacity utilisation does make costs, say, 20% higher than they would be if capacity was better matched with demand.

Still, the bigger problem for China is the coal cost. On the likely assumption that China can’t do anything to lower coal costs the country is going to be stuck with an above global average electricity underlying cost until it gets out of coal.

To be blunt, China is the world’s biggest producer of energy-intensive products by a country mile, but has higher than average energy costs.

Looking forward, the existential question

In the end, carbon concerns will force the issue. That’s been my view since about 2006 and the work since than has only deepened and strengthened my judgement on that issue and its significance. Still, knowing where the finish line is doesn’t tell you much about the journey.

The truth is that China is so big in absolute terms, and its growth rates have been so strong, that nearly any forecast can have a credible story wrapped around it. Where China will be in 2030 in terms of electricity consumption and the fuel mix is wherever you and your bias want it to be. You can make a story for coal, a story for renewables, a story for disaster, or a story of redemption. They are all possible.

ITK has a low level of confidence, but the thing we feel most confident about is that if China wants to keep growing its coal-fuelled electricity it will have to pay through the nose for the coal. That’s because developing all the new coal mines as well as replacing those that run out will cost an absolute bomb. The lack of cheap coal is the biggest constraint on the growth of coal-fuelled electricity in China at the rate that they require. We’ll return to some sums on this later.

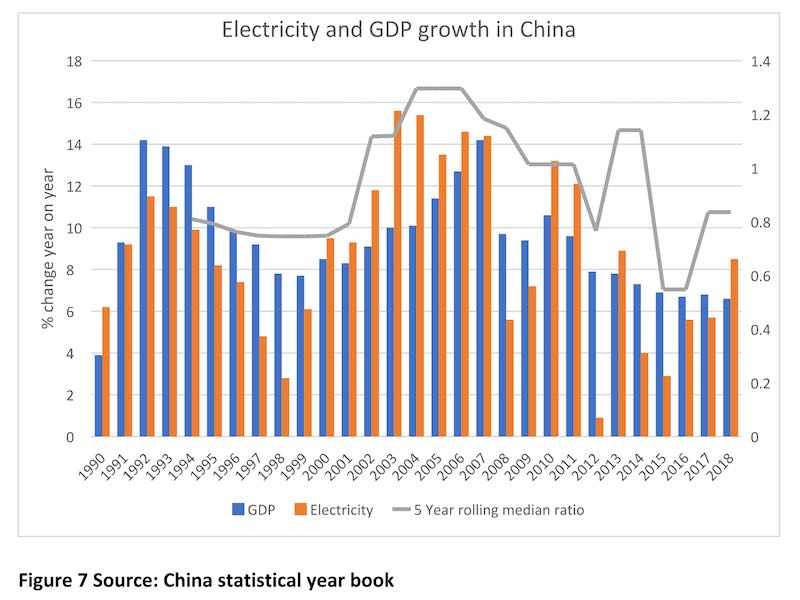

In most economies, energy intensity (energy consumption per unit of GDP) falls as the economy first industrialises and then moves to a services dominated economy.

However, in China there is no unambiguous evidence of that maturation yet. We think every 1% growth in GDP is probably about a 0.8-0.9% change in electricity consumption.

Consumption growth: Is the past a guide to the future?

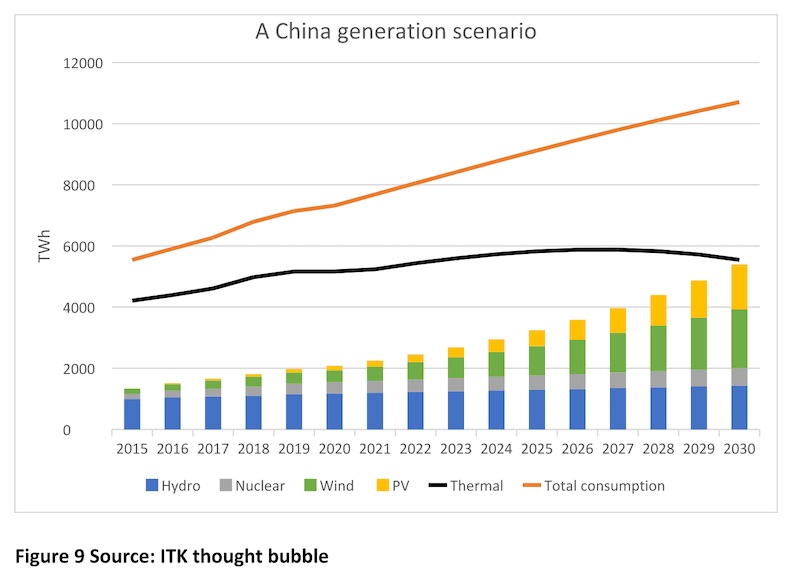

Even if electricity consumption growth in China slows down to 3-4% per year by 2030 it will have increased by, say, 3700TWh to 10700TWh. That is 50x Australia. That compares with Europe’s current consumption of 2800TWh, or the USA a bit over 4200TWh.

What industries are going to need another 3000TWh? China is already 50% of world production of steel, cement, aluminium and over 30% of plastics. Steel, cement and, to an extent, aluminium production are all tied to the construction industry. China has already achieved urbanisation for over 60% of the workforce.

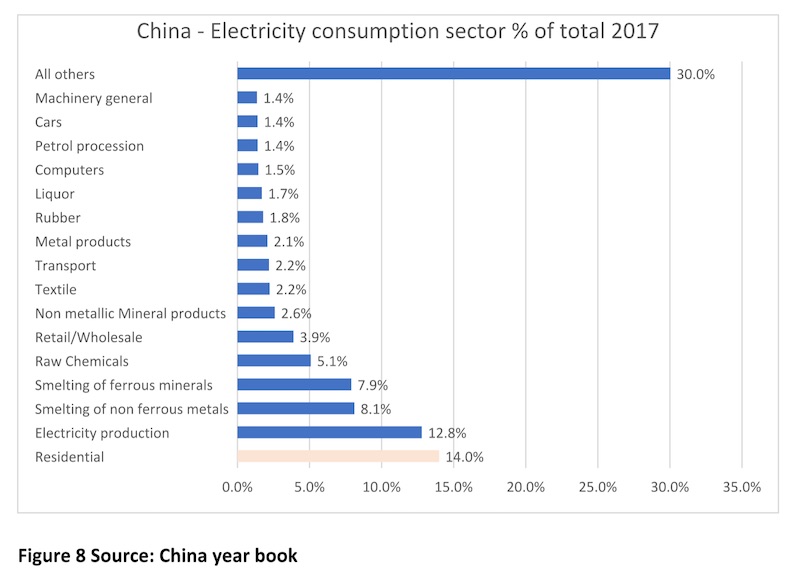

The following figure shows that, relative to many other economies, it’s the residential sector which has the main room for growth.

There will be growth in residential and in data centres, but how much? Non-ferrous metal smelting is aluminium, ferrous metal smelting is steel. Total self consumption, line losses and auxiliaries is a rather steep 13%.

There will be growth in residential and in data centres, but how much? Non-ferrous metal smelting is aluminium, ferrous metal smelting is steel. Total self consumption, line losses and auxiliaries is a rather steep 13%.

If residential consumption doubled, that would be another 900TWh. And eventually residential consumption could treble or more. So there is some growth, even without having to invoke electric cars or electricfication of industrial processes.

What we don’t see is a doubling of aluminium or steel production from these levels. If anything, we see those industries declining in China, due to high power prices, but that’s us.

Is it reasonable to see thermal share dropping to 50% by 2030?

In ITK’s view China starts from a stronger position than Australia, and Australia will certainly be over 50% by 2030, as will California and most likely Europe.

The reason China starts in a good place is because hydro is already 18%, nuclear is 5% and has some built-in growth from plants under construction – and China is the world’s leading manufacturer of wind and solar.

On top of that, China in 2020 has already, despite Covid, built 20,542km of >220 kv transmission. That compares with Australia at probably less than 10km. So they will get the required transmission done.

So in our sketch we have China build an annual average 49GW of wind and 63GW of solar, starting at less than that and building up. Nuclear also grows about 2GW per year and somehow there is a bit more hydro, but not much. Hydro loses market share. That gets thermal generation to 55% but with only very modest volume growth over the next decade.

What would that scenario mean for coal generation and coal consumption?

In the scenario we have painted, coal generation neither dies nor grows. In this doodle, coal consumption goes up about 100 mt over a decade and capacity utilisation drops about 4%. This probably wouldn’t mean that much one way or another for electricity prices.

In many ways we don’t see why China couldn’t live with a scenario like this. However, in the end it’s not enough. Far too many carbon emissions so even more is required.

In many ways we don’t see why China couldn’t live with a scenario like this. However, in the end it’s not enough. Far too many carbon emissions so even more is required.

That said, if China could get to 50% non-fossil fuel by 2030, it would be well on the way to getting the rest of the job done in the following decade.

Recommended reading:

I found this reference published Jan 2020 to be about the best thing I’d ever read on China coal generation and phasing it out. A masterpiece by Ryna Cui and 15 other contributing authors. Nothing like a well-lead team effort. https://cgs.umd.edu/research-impact/publications/high-ambition-coal-phaseout-china-feasible-strategies-through

via RenewEconomy https://ift.tt/3dwGXIX

Categories: Energy